How to navigate your funding options as a young SME dealing with the impact of COVID-19

This article was originally published on UOB Business Banking Insights by UOB on 27 April 2021.

Key Takeaways:

- Alternative funding options are quick and easy to apply for, but SMEs need to evaluate these carefully depending on their requirements and objectives

- More traditional forms of financing, such as bank loans, offer a lower interest rate than alternative funding options and might be a better option for SMEs dealing with the impact of COVID-19

In Singapore, the 2018 SME Development Survey indicated that almost 50 per cent of the SMEs surveyed cited issues such as cash flow and liquidity as a critical concern. Covid-19 has further strained liquidity and cash flow requirements.

As a young SME, the most significant task on your business radar currently is optimising your cash flow and managing liquidity to run operations smoothly and retain your workforce through this challenging period. With the emergence of additional alternative funding options, there are more ways for younger SMEs to seek funding to manage liquidity concerns.

We evaluate the pros and cons of the alternative options available to SMEs in Singapore today.

Q: What are the alternative funding options available to ease my cash flow and liquidity requirements?As a young SME, you may find yourself spoilt for choice when looking for additional working capital as many alternative funding options are emerging.

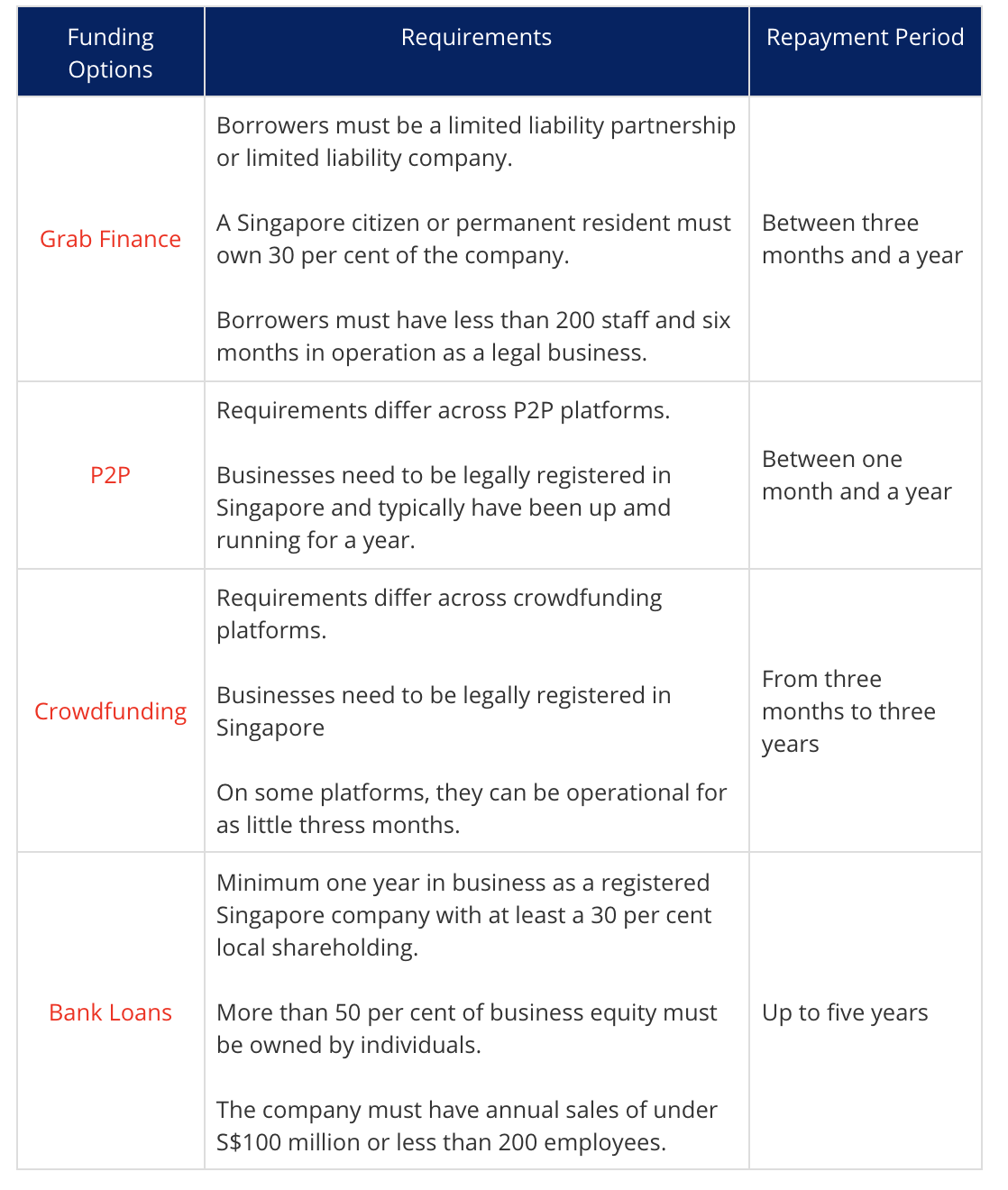

A recent addition to the funding sphere for SMEs is GrabFinance, the SME lending arm of ride-hailing company Grab. GrabFinance provides a loan quantum of up to S$100,000 to SMEs that have been in operation for at least six months. Here are some of the others.

eer-to-peer (P2P) lending:Peer-2-Peer (P2P) lending sees borrowers – such as young SMEs – secure funds directly from individual lenders. This form of funding is occasionally also referred to as Peer-2-Company (P2C) lending. One such digital financing platform, Funding Societies, hit the highest lending volume in Southeast Asia in 2019 with more than S$1 billion in SME loans. Other P2P lending platforms, such as CapitalMatch and MoolahSense, also help SMEs raise capital online outside the traditional banking system.

Crowdfunding:Used by some young SMEs and e-commerce businesses that want to validate demand for a new product, crowdfunding draws finance from outside funders. Although this approach still lacks significant traction— it is still in its early days—local platforms, such as Crowdo, are seeking to emulate overseas platforms, such as Kickstarter and Pozible.

Q: How do these alternate funding options compare with bank loans? Q: So, what are the advantages of going to an established lender?

Q: So, what are the advantages of going to an established lender?

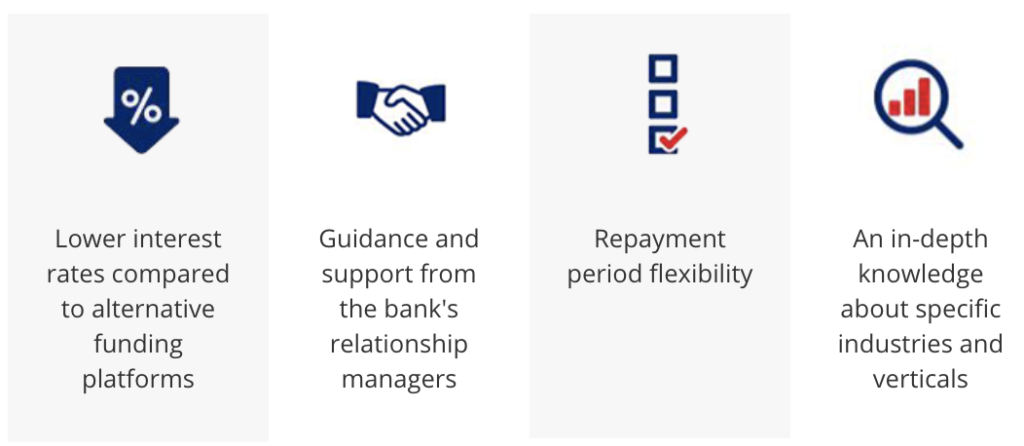

There are advantages going to an established lender like UOB. For one, banks typically offer a lower interest rate than alternative funding platforms. So, as an eligible SME, you may end up paying far higher interest payments to a P2P lender than to a bank. Also, borrowing from a bank can help build businesses’ creditworthiness.

Young SMEs that are dealing with the many complexities of running and growing a business may value the added guidance and support from a bank’s relationship manager. Banks tend to have a proven track record of working with many aspects of an SME business, from daily business banking and overdraft facilities to digital upskilling.

Furthermore, a bank usually provides a greater level of repayment period flexibility and larger loan amounts. Alternative funding providers, often acting as intermediaries, can lack this level of personalised funding support and a know-your-customer approach to the business.

UOB is committed to partnering the government to steer SMEs through these uncertain times

Use this Business Continuity Guide by Enterprise Singapore to ensure that you are

On our end, UOB has taken several steps to support SMEs during Covid-19. For example, UOB’s Business Loan aims to help fund SMEs’ plans by facilitating loans of up to S$1million, with a repayment period of up to five years and a quick response to applications within one business day.

In addition, UOB has allocated S$3 billion to provide companies financial relief at a challenging time for their business stability.

Click here to find out how UOB can help support your liquidity and business growth requirements.